October 2020

To Our Officers and Investors:

Enclosed you will find our report on the Q3 2020 performance of the Nintai Investments LLC Composite Portfolio managed by Nintai Investments LLC. Returns reflect performance since October 31 2017 when the company began operations.

Q3 2020 Returns

Last quarter we mentioned the economy and markets were marred by the constant increase in COVID infections and deaths. We stated that during Q2 we reached roughly 1,600,000 cases and 100,000 deaths - combined with high unemployment - which made deploying capital a risky venture (it’s always risky - the exception here is that uncertainty far outweighs risks). The situation in Q3 has not improved very much. By the end of Q3, total COVID cases in the US has grown to roughly 7,200,000 cases and 210,000 deaths. These numbers are simply dreadful. Until the country takes the pandemic seriously - mandatory mask wearing at all times, social distancing, limited group interactions, etc. - then the disease will continue to be a story of immense human tragedy and drag on the long term growth of the US economy. Unemployment has improved – dropping from a 24% unemployment rate to 8.4% by October 1. While coming down, that is still a shocking number which places an enormous strain on consumer spending (75% of total GDP), our social safety networks, and the service economy in general. Finally, the search for a COVID-19 vaccine is on-going, with a concern of the general public the FDA will rush approval and allow the launch of a product with an insufficient safety profile. As scientists and researchers continue to better understand the virus, it appears utilizing a herd-type immunity will be increasingly difficult to achieve. Overall, the team at Nintai finds it hard to create a risk/uncertainty model that protects to the downside while offering sufficient reward to the upside. Consequently you may see cash positions as a percent of total assets under management reach new highs.

Overall, Q3 2020 wasn’t a very successful period for our investment portfolios. We underperformed the S&P 500 by 4.97% with many holdings performing poorly. Our showing against our two other comparable indexes wasn’t as bad. We underperformed the Russell 2000 by roughly 0.87% and the MSCI ACWI ex-US by roughly 2.14%.

As we mentioned in our Q2 update, the reversion to the mean (to the downside in this case) can prove to be a taxing process. We are comfortable each portfolio holding remains financially solid, has a strong competitive position, and is led by a management team with a firm eye on investment return on capital. As you can see from our latest investment cases (mailed out last month), we remain confident that each holding should perform well over the long-term (past performance of course is no assurance of future returns). The valuation spreadsheets tell a different story. Many portfolio holdings have highly elevated valuations. In our update “When the Economy and the Markets Disagree”, I stated we are left with the quandary

of holding outstanding companies with inflated valuations. In principal, we’ve been holding onto these companies simply because we cannot replace them with any other company that we feel could compete (from a return and quality perspective) over the next decade or two. This has held us in good stead until this previous quarter. For now, we see no reason to change course and actively sell large positions out of the portfolio.

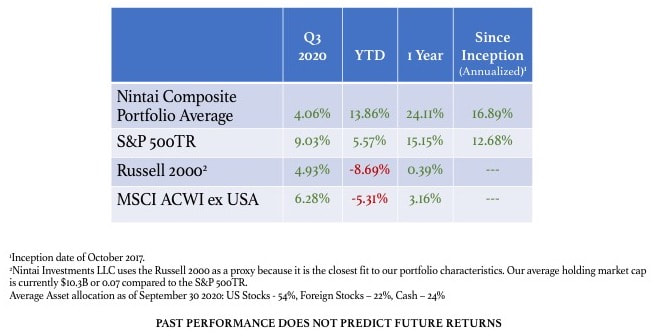

For the quarter, the Nintai Composite Portfolio generated a (+4.07%) return (including fees) versus (+8.93%) for the S&P 500, (+4.93%) for the Russell 2000, and a (+6.28%) for the MSCI ACWI ex-US Index. For the 1 Year period, the Nintai Composite Portfolio generated a (+24.11%) return (including fees) versus (+15.15%) for the S&P 500, (+0.39%) for the Russell 2000, and a (+3.16%) for the MSCI ACWI ex-US Index. Since inception (on an annualized basis), the Nintai Composite Portfolio has generated a (+17.18%) return versus the S&P 500’s (+6.91% including reinvested dividends), the Russell 2000’s (+0.83%), and the MSCI ACWI ex-US’ (+1.37%)return.

It goes without saying we are very pleased with long-term numbers, but disappointed with the quarterly returns. In last quarter’s report, we stated:

“….it should be pointed out that Nintai Investments LLC (and its predecessor Nintai Partners) typically gains its advantages in truly abysmal years. Our risk averse approach generally shines in moments of significant drawdowns in the markets.”

This certainly been the case in 2020. During Q1 (with the onset of the Corina virus pandemic), the S&P 500 achieved returns of (-0.04%) in January, (-8.23%) in February, and (-12.35%) in March. The Nintai Composite Portfolio achieved returns of (+0.68%) in January, (-6.12%) in February, and (-5.28%) in March. The portfolio outperformed the S&P 500 by a cumulative (-10.72%) to (-20.62%) respectively (or by 9.54%).

Q3 tells an entirely different story (or inverts the findings as I am fond of saying). The S&P 500 achieved returns of (+5.64%) in July, (+7.19%) in August, and (-3.80%) in September. The Nintai Composite Portfolio achieved returns of (+4.36%) in July, (+1.71%) in August, and (-1.81%) in September. The portfolio underperformed the S&P 500 by a cumulative (+4.06%) to (+9.03%) respectively (or by 4.97%).

Seen below are results for Q3 2020, year-to-date, one year, and since inception (annualized). Note we have removed the Index Blend 85% Stocks as the portfolio no longer tracks to the indexes percentages.

To Our Officers and Investors:

Enclosed you will find our report on the Q3 2020 performance of the Nintai Investments LLC Composite Portfolio managed by Nintai Investments LLC. Returns reflect performance since October 31 2017 when the company began operations.

Q3 2020 Returns

Last quarter we mentioned the economy and markets were marred by the constant increase in COVID infections and deaths. We stated that during Q2 we reached roughly 1,600,000 cases and 100,000 deaths - combined with high unemployment - which made deploying capital a risky venture (it’s always risky - the exception here is that uncertainty far outweighs risks). The situation in Q3 has not improved very much. By the end of Q3, total COVID cases in the US has grown to roughly 7,200,000 cases and 210,000 deaths. These numbers are simply dreadful. Until the country takes the pandemic seriously - mandatory mask wearing at all times, social distancing, limited group interactions, etc. - then the disease will continue to be a story of immense human tragedy and drag on the long term growth of the US economy. Unemployment has improved – dropping from a 24% unemployment rate to 8.4% by October 1. While coming down, that is still a shocking number which places an enormous strain on consumer spending (75% of total GDP), our social safety networks, and the service economy in general. Finally, the search for a COVID-19 vaccine is on-going, with a concern of the general public the FDA will rush approval and allow the launch of a product with an insufficient safety profile. As scientists and researchers continue to better understand the virus, it appears utilizing a herd-type immunity will be increasingly difficult to achieve. Overall, the team at Nintai finds it hard to create a risk/uncertainty model that protects to the downside while offering sufficient reward to the upside. Consequently you may see cash positions as a percent of total assets under management reach new highs.

Overall, Q3 2020 wasn’t a very successful period for our investment portfolios. We underperformed the S&P 500 by 4.97% with many holdings performing poorly. Our showing against our two other comparable indexes wasn’t as bad. We underperformed the Russell 2000 by roughly 0.87% and the MSCI ACWI ex-US by roughly 2.14%.

As we mentioned in our Q2 update, the reversion to the mean (to the downside in this case) can prove to be a taxing process. We are comfortable each portfolio holding remains financially solid, has a strong competitive position, and is led by a management team with a firm eye on investment return on capital. As you can see from our latest investment cases (mailed out last month), we remain confident that each holding should perform well over the long-term (past performance of course is no assurance of future returns). The valuation spreadsheets tell a different story. Many portfolio holdings have highly elevated valuations. In our update “When the Economy and the Markets Disagree”, I stated we are left with the quandary

of holding outstanding companies with inflated valuations. In principal, we’ve been holding onto these companies simply because we cannot replace them with any other company that we feel could compete (from a return and quality perspective) over the next decade or two. This has held us in good stead until this previous quarter. For now, we see no reason to change course and actively sell large positions out of the portfolio.

For the quarter, the Nintai Composite Portfolio generated a (+4.07%) return (including fees) versus (+8.93%) for the S&P 500, (+4.93%) for the Russell 2000, and a (+6.28%) for the MSCI ACWI ex-US Index. For the 1 Year period, the Nintai Composite Portfolio generated a (+24.11%) return (including fees) versus (+15.15%) for the S&P 500, (+0.39%) for the Russell 2000, and a (+3.16%) for the MSCI ACWI ex-US Index. Since inception (on an annualized basis), the Nintai Composite Portfolio has generated a (+17.18%) return versus the S&P 500’s (+6.91% including reinvested dividends), the Russell 2000’s (+0.83%), and the MSCI ACWI ex-US’ (+1.37%)return.

It goes without saying we are very pleased with long-term numbers, but disappointed with the quarterly returns. In last quarter’s report, we stated:

“….it should be pointed out that Nintai Investments LLC (and its predecessor Nintai Partners) typically gains its advantages in truly abysmal years. Our risk averse approach generally shines in moments of significant drawdowns in the markets.”

This certainly been the case in 2020. During Q1 (with the onset of the Corina virus pandemic), the S&P 500 achieved returns of (-0.04%) in January, (-8.23%) in February, and (-12.35%) in March. The Nintai Composite Portfolio achieved returns of (+0.68%) in January, (-6.12%) in February, and (-5.28%) in March. The portfolio outperformed the S&P 500 by a cumulative (-10.72%) to (-20.62%) respectively (or by 9.54%).

Q3 tells an entirely different story (or inverts the findings as I am fond of saying). The S&P 500 achieved returns of (+5.64%) in July, (+7.19%) in August, and (-3.80%) in September. The Nintai Composite Portfolio achieved returns of (+4.36%) in July, (+1.71%) in August, and (-1.81%) in September. The portfolio underperformed the S&P 500 by a cumulative (+4.06%) to (+9.03%) respectively (or by 4.97%).

Seen below are results for Q3 2020, year-to-date, one year, and since inception (annualized). Note we have removed the Index Blend 85% Stocks as the portfolio no longer tracks to the indexes percentages.

Portfolio Changes

For individual portfolio members only

Winners and Losers

For individual portfolio members only

Portfolio Characteristics

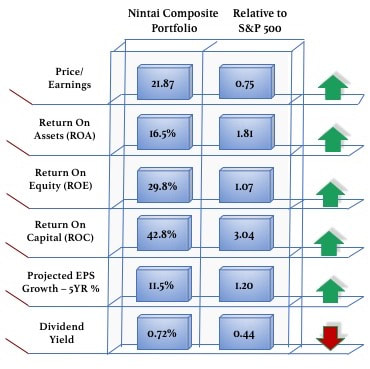

The current Abacus view as of September 2020 shows that the Nintai Composite Portfolio holdings are roughly 25% below in value to the S&P500 and projected to grow earnings at a 20% greater rate than the S&P500 over the next five years. Combining these two gives us an Abacus Comparative Value (ACV) of +45. The ACV is a simple tool which tells us how the portfolio stacks up against the S&P 500 from both a valuation and an estimated earnings growth stand point. The number shows a portfolio much cheaper in value with much greater profitability and a sharply higher projected growth. We like to see the ACV above 20, thereby giving the portfolio the best chance at outperforming the general markets.

For individual portfolio members only

Winners and Losers

For individual portfolio members only

Portfolio Characteristics

The current Abacus view as of September 2020 shows that the Nintai Composite Portfolio holdings are roughly 25% below in value to the S&P500 and projected to grow earnings at a 20% greater rate than the S&P500 over the next five years. Combining these two gives us an Abacus Comparative Value (ACV) of +45. The ACV is a simple tool which tells us how the portfolio stacks up against the S&P 500 from both a valuation and an estimated earnings growth stand point. The number shows a portfolio much cheaper in value with much greater profitability and a sharply higher projected growth. We like to see the ACV above 20, thereby giving the portfolio the best chance at outperforming the general markets.

Portfolio Industries

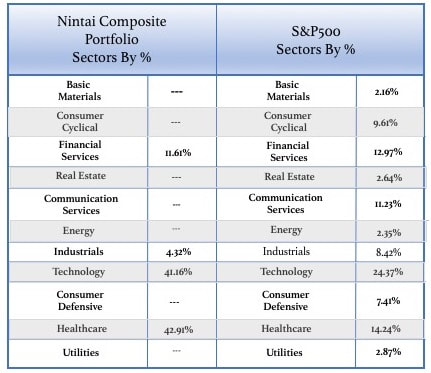

I remain highly focused in my industry and sector weightings. I currently have holdings in only 4 of the S&P 500’s 11 categories – financial services, industrials, technology and healthcare.

I remain highly focused in my industry and sector weightings. I currently have holdings in only 4 of the S&P 500’s 11 categories – financial services, industrials, technology and healthcare.

Final Thoughts

The third quarter of 2020 was the first time the Nintai Investment’s individual investment portfolios truly had a miserable performance against their proxies. As I pointed out earlier, our holdings generally outperform in down markets. This quarter represented an explosion in market enthusiasm as investors feel we turned the corner on COVID. Even with the infection of the President we are seeing this isn’t necessarily correct. There also seems to be (and we hate this phrase) an irrational exuberance in relationship to the recovery from the COVID-based recession. Again, we are in a minority that feels we have a long way to go in getting all parts of the economy back to operating on all cylinders.

Last quarter we wrote there were three main issues we felt would drive longer term returns for the markets. We think these three themes are unchanged since we first wrote about them. We have added a fourth as the United States’ approach to dealing with the COVID-19 has been woefully inadequate and will continue to be so until we get a new administration with a more systemic - and systematic - approach.

1. Stock prices - relative to price over earnings, price over cash flow, and price over estimated earnings growth - seem quite high in historical terms. While interest rates remain at historical lows, Nintai believes this doesn’t offset the full risk of such high process.

2. With over 7.45M cases (averaging roughly 35,000 new cases every day) and 212,000 deaths (averaging roughly 400 new deaths per day), the United States’ economy and overall consumer purchasing power will be severely hampered and unable to reach full potential. Any projection in earnings, growth rates, or profitability will be very hard to support until the pandemic is under control.

3. Geopolitical risks have never been higher with the US domestic political scene extremely volatile, the global energy markets in disarray, and the growth in nationalist/populist actively seeking to break up decades-old alliances. The 2020 US Presidential election only adds to these risks.

4. China represents an entirely new competitor with significant strength generated by its recent economic power, as a significant holder of US debt, and its play for greater military strength in the Pacific.

We generally don’t allow trends like these to drive our investment decisions or capital allocation. That said, the constant evolution of both US and global political economics can have an impact on individual portfolio holdings’ strategy and operations. As always, we will keep a sharp eye out for any impairment on our holdings’ valuations and/or competitive moat.

We hate underperforming. Regardless of what events that are happening in the greater economy or geopolitical world, we have no excuse for our performance in Q3 2020. You have our word we will work diligently to better our results and get back to excelling over our indexes. That said, we recognize underperformance happens and we won’t be suddenly increasing portfolio turnover to 115% or leveraging our portfolio by 400%. Rather, we will focus on what we do best and focusing on improving our process where we can.

Helping individuals and organizations achieve their life goals, support their corporate giving, or meet their retirement needs is a remarkable honor and mark of great trust. Every day we look to continue earning that trust. Should you have any questions, please do not hesitate to contact me by phone or email.

Thomas Macpherson

[email protected]

603.512.5358

My best wishes for a healthy and happy summer season.

The third quarter of 2020 was the first time the Nintai Investment’s individual investment portfolios truly had a miserable performance against their proxies. As I pointed out earlier, our holdings generally outperform in down markets. This quarter represented an explosion in market enthusiasm as investors feel we turned the corner on COVID. Even with the infection of the President we are seeing this isn’t necessarily correct. There also seems to be (and we hate this phrase) an irrational exuberance in relationship to the recovery from the COVID-based recession. Again, we are in a minority that feels we have a long way to go in getting all parts of the economy back to operating on all cylinders.

Last quarter we wrote there were three main issues we felt would drive longer term returns for the markets. We think these three themes are unchanged since we first wrote about them. We have added a fourth as the United States’ approach to dealing with the COVID-19 has been woefully inadequate and will continue to be so until we get a new administration with a more systemic - and systematic - approach.

1. Stock prices - relative to price over earnings, price over cash flow, and price over estimated earnings growth - seem quite high in historical terms. While interest rates remain at historical lows, Nintai believes this doesn’t offset the full risk of such high process.

2. With over 7.45M cases (averaging roughly 35,000 new cases every day) and 212,000 deaths (averaging roughly 400 new deaths per day), the United States’ economy and overall consumer purchasing power will be severely hampered and unable to reach full potential. Any projection in earnings, growth rates, or profitability will be very hard to support until the pandemic is under control.

3. Geopolitical risks have never been higher with the US domestic political scene extremely volatile, the global energy markets in disarray, and the growth in nationalist/populist actively seeking to break up decades-old alliances. The 2020 US Presidential election only adds to these risks.

4. China represents an entirely new competitor with significant strength generated by its recent economic power, as a significant holder of US debt, and its play for greater military strength in the Pacific.

We generally don’t allow trends like these to drive our investment decisions or capital allocation. That said, the constant evolution of both US and global political economics can have an impact on individual portfolio holdings’ strategy and operations. As always, we will keep a sharp eye out for any impairment on our holdings’ valuations and/or competitive moat.

We hate underperforming. Regardless of what events that are happening in the greater economy or geopolitical world, we have no excuse for our performance in Q3 2020. You have our word we will work diligently to better our results and get back to excelling over our indexes. That said, we recognize underperformance happens and we won’t be suddenly increasing portfolio turnover to 115% or leveraging our portfolio by 400%. Rather, we will focus on what we do best and focusing on improving our process where we can.

Helping individuals and organizations achieve their life goals, support their corporate giving, or meet their retirement needs is a remarkable honor and mark of great trust. Every day we look to continue earning that trust. Should you have any questions, please do not hesitate to contact me by phone or email.

Thomas Macpherson

[email protected]

603.512.5358

My best wishes for a healthy and happy summer season.

RSS Feed

RSS Feed