In this - part three - of a four-part series on fundamental business analysis, I will continue using SEI Investments (SEIC) as a case study taking readers through the three major components of a successful FBA. In this article, I will bring readers through the major steps in analyzing a company’s moat. This will include the major traits of the moat, how the company developed and implemented these components, and steps required to maintain or even broaden its existing moat.

It might be good to start by defining what the meaning is of a moat and its major components. I define a competitive moat as the capability of a company to outperform its competitors by achieving high returns on capital, increasing market share, and structural advantages in technology, operational efficiencies, etc. It achieves this moat with a business model that fosters these advantages over a period of 10 to 20 years. Morningstar lists five major sources of moats. These include:

Network Effect: Similar to Metcalfe’s law, the more people who use a network, the more powerful a network becomes. A great example of this Uber. The greater the amounts of drivers and riders, the more valuable the Uber network becomes.

Switching Costs: Once a company’s product becomes embedded in the business operations of customers, the harder it becomes to remove the product/system and replace with another. An example of this is electronic health records within the hospital setting. After training, development of order sets, and operational customization, switching to a new system becomes nearly impossible.

Intangible Assets: This can include patents or licenses. This assures customers must use the product or service that is legally or from a regulatory standpoint the only option. FDA approved drugs are a great example of this.

Pricing: Sometime the big guys can simply outprice the smaller guys. Just ask any local store that competes against Wal-Mart.

Sources of SEI Investments’ Moat

The company has created its moat through two product lines - TRUST 3000® and the SEI Wealth PlatformSM (the SEI Wealth Platform or the Platform). SEI owns, develops, maintains and operates these software applications and associated information processing infrastructure and facilities. Through their wholly-owned subsidiaries, they also provide business-process outsourcing services including custodial and sub-custodial services and back-office accounting services. Through its fully-integrated suite of technology and services, SEI Investments creates a turn-key offering that can be used by almost any asset management firm including private banks, trust institutions, and mutual fund companies. SEI Investments is perceived as a market leader in its technology, platform integration, breadth of offerings, and return on investment on their product and services.

Creating a Barrier to Entry

A vital aspect of SEI Investments’ competitive moat is the sheer amount of labor, dollars, and competitive intelligence that has gone into creating both TRUST 3000 and PlatformSM. Over the past 10 years it’s estimated the company has spent over $500M in product and research development. SEI Investments has increased R&D spending from 7.7% of revenue in 2015 to 10.2% in 2017. The ability of a competitor to have access to both the financial and intellectual capital to recreate these two platforms would be an extraordinarily difficult task. Once these products are launched, they are scalable to new customers at nearly no cost to SEI Investments. This creates a business model remarkably light in assets (other than the intellectual property and proprietary technology) and requires little capital to operate and create growth.

Inverting this issue, the ability of SEI Investments to operate such an asset light business allows the company to generate remarkable gross and net margins along with returns on capital. This creates excess cash thst can then be employed in expanding internal capabilities (such as increased R&D) or acquiring outside functionality or snap-on acquisitions. This virtual circle creates a deep and ever-widening moat in its competitive space.

Switching Costs and Customer Dependence

SEI Investments’ products and services are deeply embedded in the business operations of their customers. The TRUST 3000 platform is essential for asset managers to successfully manage all their securities processing and investment accounting for both domestic and foreign securities – two of the most important functions in the business. SEI Wealth Platform provides investment processing, infrastructure services, and advanced capabilities to support wealth advisory, asset management, and wealth administration functions. The Platform also provides global wealth management capabilities including a 24/7 operating model, global securities processing, and multi-currency accounting and reporting. Built around a client-centric relationship model, Wealth Platform uses an open architectural approach and supports workflow management and straight-through processing. Both of these platforms are provided in either a Software-as-a-Service or Platform-as-a-Service model.

The functionality of these two offerings mean the decision to switch out to a new vendor is neither cost-effective nor knowledge-based effective. As long as SEI Investments can maintain both a quality and functional lead, its moat is substantial from a switching cost or operational integration standpoint. The company manages or administers $920 billion in hedge, private equity, mutual fund and pooled or separately managed assets, including $339 billion in assets under management and $576 billion in client assets under administration. Putting a dime of those assets at risk is not worth it to the 8,900 clients who use SEI Investments’ products and services.

Regulatory Requirements

Anybody who has worked in the asset management business knows that state and federal regulators earn their dollars in the extent and detail of their regulatory oversight. Between the SEC, FINRA, and pertinent state regulators you better have your ducks in a row. And that ‘s not even mentioning all the overseas regulators and potential violations that can be achieved in a blink of an eye by some office in Kobe when you’re not looking. That’s where SEI Investments digs its moat even a little deeper and a little wider.

SEI Investment’s customers face an ever-changing regulatory environment. For instance, recent (and continuing) legislative activity in the United States and in other jurisdictions (including the European Union and the United Kingdom) have made and continue to make extensive changes to the laws regulating financial services firms. Recent changes include the effectiveness of the Markets in Financial Instruments Directive (MiFID II) and pending effectiveness of the General Data Protection Regulation in the European Union and the U.S. Department of Labor's Fiduciary Rule. Every one of SEI Investments’ 8.900 clients know that the company’s products and services have to reflect these changes every day. There aren’t any competitors with the intellectual knowledge base, skill sets, regulatory knowledge, and technical abilities to update their product and service offerings on such a regular basis.

Conclusions

A solid fundamental business analysis will dig deep into understanding how and why a potential portfolio holding has a competitive advantage. The ability to tie in knowledge about competitors, product and service offerings, customer segmentation business needs, regulatory requirements, and the company’s financial strength to maintain and extend its moat is vital. Without this understanding, it’s difficult to predict how successful this potential investment might be in 10 to 20 years. Is the fundamental business analysis process a perfect predictor? Certainly not. Will it help you understand the potential ability of the company to create long-term value? Sometimes. But one thing is certain. It is unlikely to hurt in developing your understanding of the company’s business case.

In the last part of this series, I will finish with researching the capabilities of a company to both produce and manage long-term growth. Until then, I look forward to your thoughts and comments.

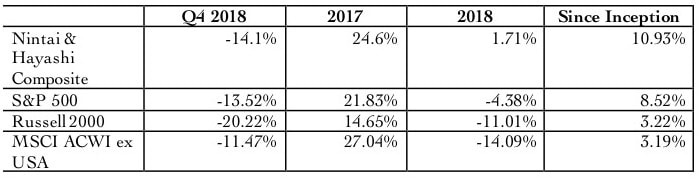

DISCLOSURE: I currently own SEI Investments in individual investment accounts at Nintai Investments LLC as well as the Hayashi Foundation.

It might be good to start by defining what the meaning is of a moat and its major components. I define a competitive moat as the capability of a company to outperform its competitors by achieving high returns on capital, increasing market share, and structural advantages in technology, operational efficiencies, etc. It achieves this moat with a business model that fosters these advantages over a period of 10 to 20 years. Morningstar lists five major sources of moats. These include:

Network Effect: Similar to Metcalfe’s law, the more people who use a network, the more powerful a network becomes. A great example of this Uber. The greater the amounts of drivers and riders, the more valuable the Uber network becomes.

Switching Costs: Once a company’s product becomes embedded in the business operations of customers, the harder it becomes to remove the product/system and replace with another. An example of this is electronic health records within the hospital setting. After training, development of order sets, and operational customization, switching to a new system becomes nearly impossible.

Intangible Assets: This can include patents or licenses. This assures customers must use the product or service that is legally or from a regulatory standpoint the only option. FDA approved drugs are a great example of this.

Pricing: Sometime the big guys can simply outprice the smaller guys. Just ask any local store that competes against Wal-Mart.

Sources of SEI Investments’ Moat

The company has created its moat through two product lines - TRUST 3000® and the SEI Wealth PlatformSM (the SEI Wealth Platform or the Platform). SEI owns, develops, maintains and operates these software applications and associated information processing infrastructure and facilities. Through their wholly-owned subsidiaries, they also provide business-process outsourcing services including custodial and sub-custodial services and back-office accounting services. Through its fully-integrated suite of technology and services, SEI Investments creates a turn-key offering that can be used by almost any asset management firm including private banks, trust institutions, and mutual fund companies. SEI Investments is perceived as a market leader in its technology, platform integration, breadth of offerings, and return on investment on their product and services.

Creating a Barrier to Entry

A vital aspect of SEI Investments’ competitive moat is the sheer amount of labor, dollars, and competitive intelligence that has gone into creating both TRUST 3000 and PlatformSM. Over the past 10 years it’s estimated the company has spent over $500M in product and research development. SEI Investments has increased R&D spending from 7.7% of revenue in 2015 to 10.2% in 2017. The ability of a competitor to have access to both the financial and intellectual capital to recreate these two platforms would be an extraordinarily difficult task. Once these products are launched, they are scalable to new customers at nearly no cost to SEI Investments. This creates a business model remarkably light in assets (other than the intellectual property and proprietary technology) and requires little capital to operate and create growth.

Inverting this issue, the ability of SEI Investments to operate such an asset light business allows the company to generate remarkable gross and net margins along with returns on capital. This creates excess cash thst can then be employed in expanding internal capabilities (such as increased R&D) or acquiring outside functionality or snap-on acquisitions. This virtual circle creates a deep and ever-widening moat in its competitive space.

Switching Costs and Customer Dependence

SEI Investments’ products and services are deeply embedded in the business operations of their customers. The TRUST 3000 platform is essential for asset managers to successfully manage all their securities processing and investment accounting for both domestic and foreign securities – two of the most important functions in the business. SEI Wealth Platform provides investment processing, infrastructure services, and advanced capabilities to support wealth advisory, asset management, and wealth administration functions. The Platform also provides global wealth management capabilities including a 24/7 operating model, global securities processing, and multi-currency accounting and reporting. Built around a client-centric relationship model, Wealth Platform uses an open architectural approach and supports workflow management and straight-through processing. Both of these platforms are provided in either a Software-as-a-Service or Platform-as-a-Service model.

The functionality of these two offerings mean the decision to switch out to a new vendor is neither cost-effective nor knowledge-based effective. As long as SEI Investments can maintain both a quality and functional lead, its moat is substantial from a switching cost or operational integration standpoint. The company manages or administers $920 billion in hedge, private equity, mutual fund and pooled or separately managed assets, including $339 billion in assets under management and $576 billion in client assets under administration. Putting a dime of those assets at risk is not worth it to the 8,900 clients who use SEI Investments’ products and services.

Regulatory Requirements

Anybody who has worked in the asset management business knows that state and federal regulators earn their dollars in the extent and detail of their regulatory oversight. Between the SEC, FINRA, and pertinent state regulators you better have your ducks in a row. And that ‘s not even mentioning all the overseas regulators and potential violations that can be achieved in a blink of an eye by some office in Kobe when you’re not looking. That’s where SEI Investments digs its moat even a little deeper and a little wider.

SEI Investment’s customers face an ever-changing regulatory environment. For instance, recent (and continuing) legislative activity in the United States and in other jurisdictions (including the European Union and the United Kingdom) have made and continue to make extensive changes to the laws regulating financial services firms. Recent changes include the effectiveness of the Markets in Financial Instruments Directive (MiFID II) and pending effectiveness of the General Data Protection Regulation in the European Union and the U.S. Department of Labor's Fiduciary Rule. Every one of SEI Investments’ 8.900 clients know that the company’s products and services have to reflect these changes every day. There aren’t any competitors with the intellectual knowledge base, skill sets, regulatory knowledge, and technical abilities to update their product and service offerings on such a regular basis.

Conclusions

A solid fundamental business analysis will dig deep into understanding how and why a potential portfolio holding has a competitive advantage. The ability to tie in knowledge about competitors, product and service offerings, customer segmentation business needs, regulatory requirements, and the company’s financial strength to maintain and extend its moat is vital. Without this understanding, it’s difficult to predict how successful this potential investment might be in 10 to 20 years. Is the fundamental business analysis process a perfect predictor? Certainly not. Will it help you understand the potential ability of the company to create long-term value? Sometimes. But one thing is certain. It is unlikely to hurt in developing your understanding of the company’s business case.

In the last part of this series, I will finish with researching the capabilities of a company to both produce and manage long-term growth. Until then, I look forward to your thoughts and comments.

DISCLOSURE: I currently own SEI Investments in individual investment accounts at Nintai Investments LLC as well as the Hayashi Foundation.

RSS Feed

RSS Feed