This year was truly a year of change at Nintai. Not only have we closed down our management consulting arm and internal fund, but we have created the Nintai Charitable Trust of which my current positions of Nintai Partners will be transferred. In addition, 2015 was a huge transition for our holdings. We have said goodbye to roughly 40% of the companies we owned at the beginning of the year such as FactSet Research (NYSE:FDS) and Manhattan Associates (NASDAQ:MANH). On the other side of the proverbial balance sheet, we have added holdings that we are truly excited about and expect to partner with for the long term. These include CBOE Holdings (NASDAQ:CBOE), Collectors Universe (NASDAQ:CLCT), Computer Modeling Group (TSK:CMG), Computer Systems and Programs (NASDAQ:CPSI), and SolarWinds (NYSE:SWI). Nearly all our decisions were based on valuation alone where we have focused on selling at high valuations and replacing at much lower valuations. In two areas we will not compromise: buying at a significant discount to fair value and the quality of the company’s financials/returns.

That having been said, we simply haven’t found opportunities to replace our sales, and our cash position ballooned to roughly 20% by end of last week. The past few days have - as one writer once eloquently said - “made the ears of the wolf twitch”. We love days like the past two. Mass selling can provide great opportunities in mispricing and yesterday we were happy to find one. It didn't make much of a dent in our cash position, but we are happy to put capital to work with such a company.

Linear Technology (NASDAQ:LLTC): Purchase

If you can believe, Linear has been on our watch list since 2004 (we almost purchased in 2009 but simply didn't have the cash having purchased several other positions at far deeper discounts). After updating our estimated intrinsic value in February 2015, we placed a limit order at $39.50/share. Management recently shared concerns about the September quarter speaking of broader economic issues rather than company specific problems. Combine this with the sudden drop in the past few days, and the stock price briefly touched our ask price and we became owners in the company. We couldn't be more pleased.

Linear is the type of company we love to purchase and hold for as long Mr. Market will allow. The company is the leader in high-performance analog (HPA) chips. These require extreme precision and very high reliability in devices used across multiple sectors. Currently, their highest need is in the automobile and industrial sectors. Because of the stress on reliability of the chip (combined with the small cost related to the entire piece of equipment), many of Linear’s clients are happy to pay top dollar for their chips. What we truly love about Linear’s chips is their long product life helping the business maintain extraordinarily low capital requirements. The inability for other competitors to create similar chips at cheaper prices, the depth of Linear’s relationships with key customers, and the skill of their work force give the company a wide competitive moat in our opinion.

We are also very impressed with Linear’s management. They have done an extraordinary job at maintaining a laser-like focus on the very profitable HPA market. They are quite willing to let projects go by if clients are unwilling to recognize the value of Linear’s product quality. With gross and net margins of 76% and 35% respectively, management has demonstrated their commitment to long-term profitability. In addition, over the past five years the company has generated an average ROE of 80%, free cash flow/total sales of 40%, and ROC of 38%. This is a company that is a true cash machine. Finally, the company has no short or long term debt, $1.2 billion of cash on the balance sheet and yields roughly 3%. Utilizing a DCF model, we believe shares of LLTC are worth roughly $49/share or trade at roughly a 22% discount to fair value.

Portfolio Positioning

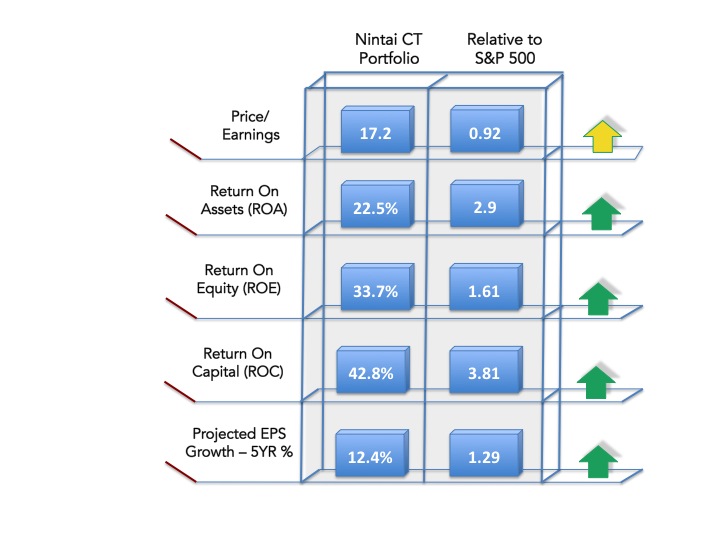

After all of these portfolio changes, the Nintai Charitable Trust is somewhat cheaper than the S&P500 Index, far more profitable, and is estimated to grow at roughly 30% faster than the S&P500.

That having been said, we simply haven’t found opportunities to replace our sales, and our cash position ballooned to roughly 20% by end of last week. The past few days have - as one writer once eloquently said - “made the ears of the wolf twitch”. We love days like the past two. Mass selling can provide great opportunities in mispricing and yesterday we were happy to find one. It didn't make much of a dent in our cash position, but we are happy to put capital to work with such a company.

Linear Technology (NASDAQ:LLTC): Purchase

If you can believe, Linear has been on our watch list since 2004 (we almost purchased in 2009 but simply didn't have the cash having purchased several other positions at far deeper discounts). After updating our estimated intrinsic value in February 2015, we placed a limit order at $39.50/share. Management recently shared concerns about the September quarter speaking of broader economic issues rather than company specific problems. Combine this with the sudden drop in the past few days, and the stock price briefly touched our ask price and we became owners in the company. We couldn't be more pleased.

Linear is the type of company we love to purchase and hold for as long Mr. Market will allow. The company is the leader in high-performance analog (HPA) chips. These require extreme precision and very high reliability in devices used across multiple sectors. Currently, their highest need is in the automobile and industrial sectors. Because of the stress on reliability of the chip (combined with the small cost related to the entire piece of equipment), many of Linear’s clients are happy to pay top dollar for their chips. What we truly love about Linear’s chips is their long product life helping the business maintain extraordinarily low capital requirements. The inability for other competitors to create similar chips at cheaper prices, the depth of Linear’s relationships with key customers, and the skill of their work force give the company a wide competitive moat in our opinion.

We are also very impressed with Linear’s management. They have done an extraordinary job at maintaining a laser-like focus on the very profitable HPA market. They are quite willing to let projects go by if clients are unwilling to recognize the value of Linear’s product quality. With gross and net margins of 76% and 35% respectively, management has demonstrated their commitment to long-term profitability. In addition, over the past five years the company has generated an average ROE of 80%, free cash flow/total sales of 40%, and ROC of 38%. This is a company that is a true cash machine. Finally, the company has no short or long term debt, $1.2 billion of cash on the balance sheet and yields roughly 3%. Utilizing a DCF model, we believe shares of LLTC are worth roughly $49/share or trade at roughly a 22% discount to fair value.

Portfolio Positioning

After all of these portfolio changes, the Nintai Charitable Trust is somewhat cheaper than the S&P500 Index, far more profitable, and is estimated to grow at roughly 30% faster than the S&P500.

After making these changes (producing an alarming turnover rate YTD of 47%) we are quite comfortable to sit back and let our portfolio companies and management do the heavy lifting in the future. We believe we are positioned to achieve signifiant compunding returns if we remain patient and diligent in our investment practices.

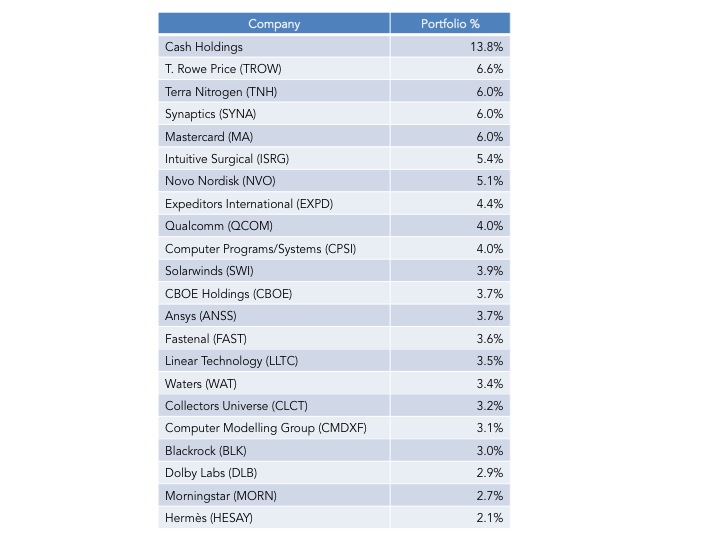

The Trust's current portfolio positions and weightings are as follows:

The Trust's current portfolio positions and weightings are as follows:

As always, we look forward to your thoughts and comments.

**Please note this article reflects my personal holdings in the Nintai Charitable Trust. Opinions expressed in this article are related to the Nintai Charitable Trust and the Trust alone. **

**Please note this article reflects my personal holdings in the Nintai Charitable Trust. Opinions expressed in this article are related to the Nintai Charitable Trust and the Trust alone. **

RSS Feed

RSS Feed