Our recent purchase of Intuitive Surgical (ISRG) has prompted many of our readers to question the investment case – and in particular the margin of safety – behind the transaction. These are great questions that force us to describe and justify our methodology and question our assumptions. We greatly appreciate the feedback.

Since Ben Graham’s first wrote about his concept of “margin of safety”, there has been a general consensus about the definition of the term. We think Seth Klarman said it best when he stated that a margin of safety “is achieved when securities are purchased at prices sufficiently below underlying value to allow for human error, bad luck, or extreme volatility in a complex, unpredictable and rapidly changing world”[1]. For most value investors, the idea of utilizing margin of safety as the bedrock for their investment process is essential to their success. The idea of a value guru purchasing an investment at a price equal to or exceeding its fair value is so flawed as to be ludicrous in nature.

That said, defining what is an adequate margin of safety is something that remains uniquely personal for each value investor. Some investors use percentages (“at least a 25% discount to estimated intrinsic value”) while others might use a multiple (“less than 3 x enterprise value as calculated by recent M&A activity”). Nintai is no different. We employ a unique process that allows for a customized approach to every investment opportunity.

Nintai’s Requirements: Margin of Safety

First, we should emphasize that margin of safety as a concept is never negotiable in our investment process. We will never pay fair value for a prospective holding. That said, how much of a margin of safety is flexible and is dependent upon multiple investment characteristics and certain market dynamics. When calculating an appropriate margin of safety, Nintai uses both specific corporate data as well as risk/uncertainty trends to assess the size of the margin required for investment. As many readers asked questions about our purchase of Intuitive Surgical (ISRG) last week, we thought we’d use the company as a use case in today’s article.

1. Corporate Measures: Impact on Margin of Safety

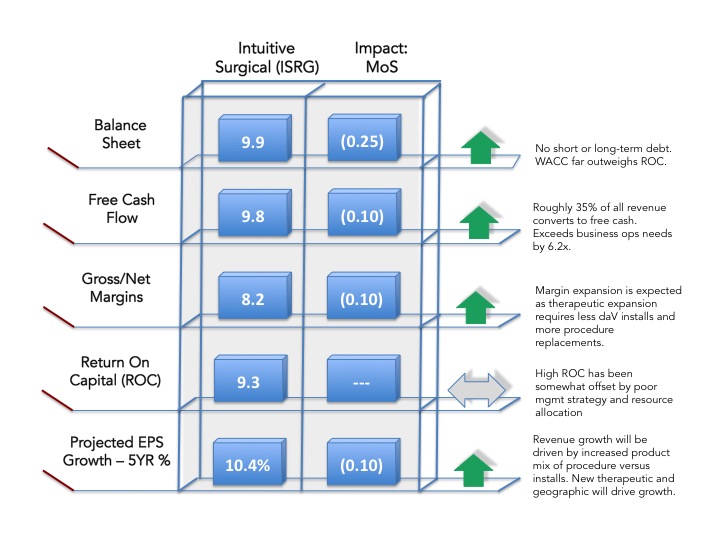

To assign what we think is an appropriate margin of safety in our investments, we begin with key corporate measures. These include the strength of the balance sheet, percentage of revenue converted to free cash, trend of gross and net margins, return on capital, and the strength/makeup of earnings growth over the next five years (amongst many others).

Seen below is a Nintai Abacus report outlining the value assigned to some of the criteria (1 being worst and 10 being the best) and its impact on the margin of safety. For example, ISRG’s balance sheet receives a score of 9.9 with no short or long-term debt and reduces the margin of safety required by 0.25%. Overall, this screen represents 5 corporate criteria which taken in total reduce the required margin of safety by 0.55%.

Since Ben Graham’s first wrote about his concept of “margin of safety”, there has been a general consensus about the definition of the term. We think Seth Klarman said it best when he stated that a margin of safety “is achieved when securities are purchased at prices sufficiently below underlying value to allow for human error, bad luck, or extreme volatility in a complex, unpredictable and rapidly changing world”[1]. For most value investors, the idea of utilizing margin of safety as the bedrock for their investment process is essential to their success. The idea of a value guru purchasing an investment at a price equal to or exceeding its fair value is so flawed as to be ludicrous in nature.

That said, defining what is an adequate margin of safety is something that remains uniquely personal for each value investor. Some investors use percentages (“at least a 25% discount to estimated intrinsic value”) while others might use a multiple (“less than 3 x enterprise value as calculated by recent M&A activity”). Nintai is no different. We employ a unique process that allows for a customized approach to every investment opportunity.

Nintai’s Requirements: Margin of Safety

First, we should emphasize that margin of safety as a concept is never negotiable in our investment process. We will never pay fair value for a prospective holding. That said, how much of a margin of safety is flexible and is dependent upon multiple investment characteristics and certain market dynamics. When calculating an appropriate margin of safety, Nintai uses both specific corporate data as well as risk/uncertainty trends to assess the size of the margin required for investment. As many readers asked questions about our purchase of Intuitive Surgical (ISRG) last week, we thought we’d use the company as a use case in today’s article.

1. Corporate Measures: Impact on Margin of Safety

To assign what we think is an appropriate margin of safety in our investments, we begin with key corporate measures. These include the strength of the balance sheet, percentage of revenue converted to free cash, trend of gross and net margins, return on capital, and the strength/makeup of earnings growth over the next five years (amongst many others).

Seen below is a Nintai Abacus report outlining the value assigned to some of the criteria (1 being worst and 10 being the best) and its impact on the margin of safety. For example, ISRG’s balance sheet receives a score of 9.9 with no short or long-term debt and reduces the margin of safety required by 0.25%. Overall, this screen represents 5 corporate criteria which taken in total reduce the required margin of safety by 0.55%.

At Nintai, we use a total of 17 corporate criteria that can impact the required margin of safety by up to 5% in total.

2. Risk and Uncertainty Measures: Impact on Margin of Safety

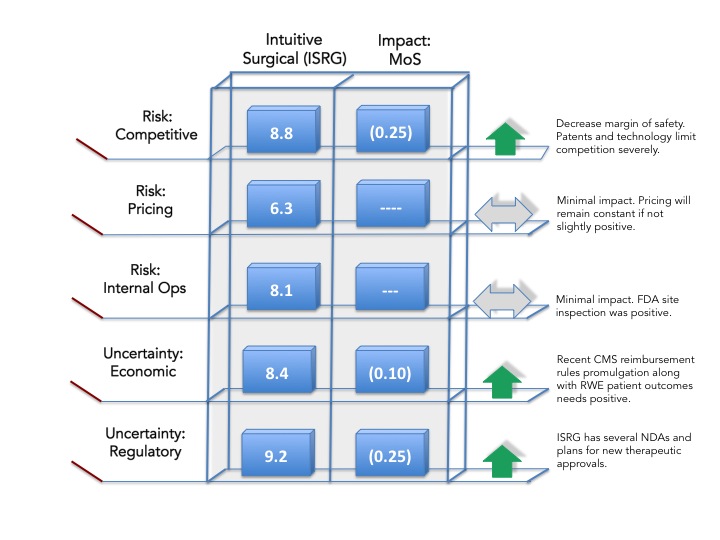

In addition to certain corporate criteria, Nintai looks at multiple characteristics surrounding risk and uncertainty that might impact our required margin of safety. Seen below is the Nintai Abacus report outlining the value assigned to the criteria (1 being worst and 10 being the best) and its impact on the margin of safety. For example, ISRG’s risk relative to competition rates an 8.8 reflecting the failure of two competitors to achieve gold standard of care in their respective therapeutic groups as well as the failure of a third competitor to achieve its primary endpoints in a study for their product. This score reduces the margin of safety required by 0.25%.

2. Risk and Uncertainty Measures: Impact on Margin of Safety

In addition to certain corporate criteria, Nintai looks at multiple characteristics surrounding risk and uncertainty that might impact our required margin of safety. Seen below is the Nintai Abacus report outlining the value assigned to the criteria (1 being worst and 10 being the best) and its impact on the margin of safety. For example, ISRG’s risk relative to competition rates an 8.8 reflecting the failure of two competitors to achieve gold standard of care in their respective therapeutic groups as well as the failure of a third competitor to achieve its primary endpoints in a study for their product. This score reduces the margin of safety required by 0.25%.

At Nintai, we use a total of 12 risk/uncertainty criteria that can impact the required margin of safety by up to 3% in total.

Conclusions

At Nintai we don’t have a set margin of safety (25% below estimated intrinsic value) that we require, but rather a process that looks to quantify the best estimate by individual company. By no means is this process static. When we review each holding on a quarterly basis, we will reevaluate each and every characteristic. We recognize this process is time consuming and requires extensive knowledge, data, and industrial expertise. With such a focused portfolio, we believe the process requires such an intricate methodology. Overall, we believe our long-term performance bears out the value of such a process. We hope this answers some of the great questions we received over the past week.

As always, we look forward to your thoughts and comments.

Conclusions

At Nintai we don’t have a set margin of safety (25% below estimated intrinsic value) that we require, but rather a process that looks to quantify the best estimate by individual company. By no means is this process static. When we review each holding on a quarterly basis, we will reevaluate each and every characteristic. We recognize this process is time consuming and requires extensive knowledge, data, and industrial expertise. With such a focused portfolio, we believe the process requires such an intricate methodology. Overall, we believe our long-term performance bears out the value of such a process. We hope this answers some of the great questions we received over the past week.

As always, we look forward to your thoughts and comments.

RSS Feed

RSS Feed