For centuries, the Fata Morgana - a mirage created by refracted light - caused varying amounts of fear, panic, and wonder to sailors around the world. Named after King Arthur’s sister Morgana (who lived in a crystal city under the sea that would occasionally surface), sailors would record seeing everything from armies fighting battles to huge fleets crossing the ocean. The fata morgana - of course - would eventually be explained by understanding how light is refracted through different temperature layers. What sailors saw was a combination of such refraction with a (un)healthy dose of creative imagination.

I bring up the Fata Morgana because it isn’t just sailors who see mirages in the distance. Investors can as well. For instance, the vast majority of income investors see most business loans as refracted through 20th century lenses. They see loans backed up by collateral with credit ratings providing a certain guidance on risk. Much like the mortgage-backed securities (MBS) market of 2005-2007, this couldn’t be a larger mirage. Since 2011, there has been an explosion of Cov-lite loans in both dollars and as a total percentage of leveraged loans.

Covenant Light (Cov-lite) loans are loans that don’t contain the more traditional covenants that protect a lender against potential loss. In earlier times, banks would require certain collateral (such as your house against a mortgage) that would allow them to seize control of assets or intervene in operations if the underlying assets lose enough value. The key here is the bank could see a developing situation and take corrective action before things got too far out of control. Generally these covenants fit into three buckets. The first is leverage. This is generally calculated as a multiple of either income statement or balance sheet line items. Second is loan-to-value. This is the ratio of a loan to the value of an asset purchased. The last is an EBITDA (earnings before interest, taxes, depreciation, and amortization) ratio. This covenant might be expressed as EBITDA as a percent of total revenue.

Cov-lite loans dispense with all of this. These loans are generally made by a syndicate of banks with little to no covenants attached to the loan. The lender has little protection against loss. The market for Cov-lite loans has been driven by private equity and their use of such loans. As these firms have played an ever increasing role in corporate debt financing, lower credit quality companies have used this to force banks to give way on the more traditional loans guarded by the series of covenants previously discussed. Cov-lite loans are considered leveraged loans or loans provided to companies/individuals with significant debt already or poor credit quality. Many leveraged loans are utilized for leveraged buy outs (LBOs) mergers and acquisitions, or restructuring the balance sheet.

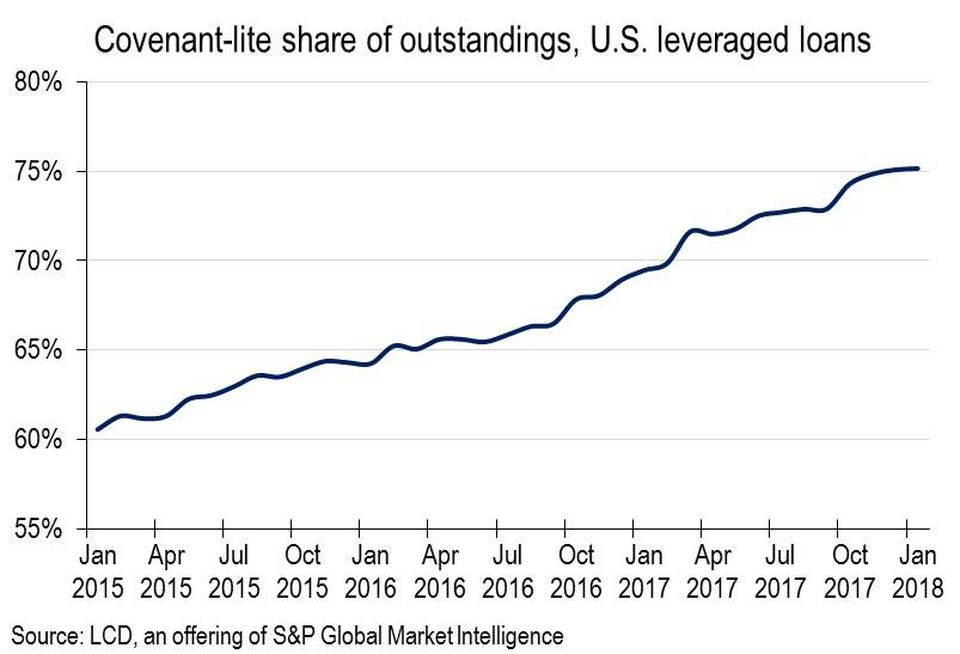

Cov-lite loans peaked just before the Lehman crash in 2007 at roughly $94B. After that, the loans essentially dried up with only $2B in 2008, $4B in 2009, and $8B in 2010 before roaring back to $58B in 2011. Fast forward to 2018 when nearly 75% of the $970B leveraged loan market is made up of Cov-lite loans or roughly $728B in corporate debt. (See chart below) Compare this to the $94B before the Lehman crash and one begins to feel the palms sweat a little bit.

This growth - in both dollars and percentage - of total leveraged loans have several effects on the corporate debt markets.

Hard to See the Incoming Train with Cov-lite

Traditionally, covenant loans provided lenders with warnings to potential impairment or losses. When a company began to close in on an EBITDA ratio cap, the bank would be notified and prepare itself to either renegotiate the loan or take steps to protect its capital. Cov-lite loans rob banks (no pun intended) of the ability to get ahead of the curve and protect their capital. Should there be a slowdown in the general economy, many syndicates could be blind-sided by wide-spread defaults.

A Majority of Cov-lite are B3 Companies

In 2018, nearly half (or roughly $360B) of all Cov-lite loans were made to companies with credit ratings of B3. This means that a drop of one notch in credit quality will bring these loans into junk status. This kind of mass movement can play old Harry with bond funds whose covenants may require these loans be removed from their portfolios. For individual investors, this could lead to significant drops in the NAV of their corporate debt funds.

Cov-lite Can Be Good and Bad for Equity Investors

For investors in companies with lower credit quality, Cov-lite loans might actually be a net positive since the lender has little or no protection should there be slow down. Rather than face dramatic steps such as corporate restructuring or asset seizure, the company may be able to face little action. That said, it should be pointed out that if the company has a.) poor credit quality and b.) slowing or failing business fundamentals then it is unlikely a Cov-lite loan versus a covenant-based loan will save their investment.

Why This Matters

As a value investor, I see my top priority as avoiding the permanent impairment of my investors’ capital. Growth is necessary as well, but certainly not my top priority. The leveraged loan market – frequently mixed with the High-Yield or Junk Bond markets – can tantalize investors with generous dividend yields. As a value investor with very strict balance sheet requirements, Cov-lite supported companies play no role in my portfolio selection. For those who do invest in such companies, they should go into the investment with their eyes wide open and aware of several risks.

Things Can Go From Fine to Very Bad Quite Quickly

Much like recessions - when you don’t know it’s coming until you are in one - the Cov-lite loan market can head south quite quickly. For instance, S&P Global Market Intelligence reports that earnings-per-share growth across the Cov-lite market in the first quarter 2019 dropped to 0.5%, from 14% in the fourth quarter of 2018, and from growth rates of 20%–25% over the first three quarters of 2018. Default rates of Cov-lite rates went from 0.2% in June 2007 to 10% in December 2007 - a grand total of 6 months.

Cov-Lite Market Liquidity can Disappear Quickly

During the height of the credit crisis in 2008, there was simply no market for Cov-lite paper. It seemed that in a matter of moments the trading market was fine and then closed to investors. For those who didn’t need the cash thrown off from these investments, a year later the market (though much smaller) was working efficiently. However, open-ended funds that had significant withdrawals saw their investors suffer horrendous losses. In addition, companies that survived on Cov-lite loans saw their financing dry up and frequently sought bankruptcy protection.

Risk is Often Mis-Priced and Difficult to Value

It seems to me the lower credit quality markets either trade at exuberant rates or severely depressed rates. Much like Goldilocks of yore, the temperature never seems to be just right. Additionally, delving into the actual loan agreements and understanding the legal obligations of both parties takes a mind far smarter than I and trained in corporate law. It’s extremely easy for a layman to misprice risk in these markets.

Conclusions

Whenever markets reach highs and valuations are stretched, the first thing I look for are opportunities where I might be mispricing and/or misunderstanding risk in my portfolios. This type of risk can be direct (owning an individual company dependent on short-term paper to fund operations) or indirect (owning an individual company with widespread exposure to such companies) dependent upon the company. Because Nintai Investments steers clear of lower credit quality holdings and does not invest in debt instruments of any sort, we remain comfortable the explosion in leveraged loans will have minimum direct impact on our portfolio performance. Indirect impact - such as when the credit markets seize up and stock prices across the board collapse - is a whole other issue. For those investors who are invested - in either direct or indirect ways - in the leverage loan markets or individual companies dependent on such loans, we advise caution. Sometimes the illusion created by fata morgana creates castles where none exist and that’s not a proper defense for anybody’s investments.

Hard to See the Incoming Train with Cov-lite

Traditionally, covenant loans provided lenders with warnings to potential impairment or losses. When a company began to close in on an EBITDA ratio cap, the bank would be notified and prepare itself to either renegotiate the loan or take steps to protect its capital. Cov-lite loans rob banks (no pun intended) of the ability to get ahead of the curve and protect their capital. Should there be a slowdown in the general economy, many syndicates could be blind-sided by wide-spread defaults.

A Majority of Cov-lite are B3 Companies

In 2018, nearly half (or roughly $360B) of all Cov-lite loans were made to companies with credit ratings of B3. This means that a drop of one notch in credit quality will bring these loans into junk status. This kind of mass movement can play old Harry with bond funds whose covenants may require these loans be removed from their portfolios. For individual investors, this could lead to significant drops in the NAV of their corporate debt funds.

Cov-lite Can Be Good and Bad for Equity Investors

For investors in companies with lower credit quality, Cov-lite loans might actually be a net positive since the lender has little or no protection should there be slow down. Rather than face dramatic steps such as corporate restructuring or asset seizure, the company may be able to face little action. That said, it should be pointed out that if the company has a.) poor credit quality and b.) slowing or failing business fundamentals then it is unlikely a Cov-lite loan versus a covenant-based loan will save their investment.

Why This Matters

As a value investor, I see my top priority as avoiding the permanent impairment of my investors’ capital. Growth is necessary as well, but certainly not my top priority. The leveraged loan market – frequently mixed with the High-Yield or Junk Bond markets – can tantalize investors with generous dividend yields. As a value investor with very strict balance sheet requirements, Cov-lite supported companies play no role in my portfolio selection. For those who do invest in such companies, they should go into the investment with their eyes wide open and aware of several risks.

Things Can Go From Fine to Very Bad Quite Quickly

Much like recessions - when you don’t know it’s coming until you are in one - the Cov-lite loan market can head south quite quickly. For instance, S&P Global Market Intelligence reports that earnings-per-share growth across the Cov-lite market in the first quarter 2019 dropped to 0.5%, from 14% in the fourth quarter of 2018, and from growth rates of 20%–25% over the first three quarters of 2018. Default rates of Cov-lite rates went from 0.2% in June 2007 to 10% in December 2007 - a grand total of 6 months.

Cov-Lite Market Liquidity can Disappear Quickly

During the height of the credit crisis in 2008, there was simply no market for Cov-lite paper. It seemed that in a matter of moments the trading market was fine and then closed to investors. For those who didn’t need the cash thrown off from these investments, a year later the market (though much smaller) was working efficiently. However, open-ended funds that had significant withdrawals saw their investors suffer horrendous losses. In addition, companies that survived on Cov-lite loans saw their financing dry up and frequently sought bankruptcy protection.

Risk is Often Mis-Priced and Difficult to Value

It seems to me the lower credit quality markets either trade at exuberant rates or severely depressed rates. Much like Goldilocks of yore, the temperature never seems to be just right. Additionally, delving into the actual loan agreements and understanding the legal obligations of both parties takes a mind far smarter than I and trained in corporate law. It’s extremely easy for a layman to misprice risk in these markets.

Conclusions

Whenever markets reach highs and valuations are stretched, the first thing I look for are opportunities where I might be mispricing and/or misunderstanding risk in my portfolios. This type of risk can be direct (owning an individual company dependent on short-term paper to fund operations) or indirect (owning an individual company with widespread exposure to such companies) dependent upon the company. Because Nintai Investments steers clear of lower credit quality holdings and does not invest in debt instruments of any sort, we remain comfortable the explosion in leveraged loans will have minimum direct impact on our portfolio performance. Indirect impact - such as when the credit markets seize up and stock prices across the board collapse - is a whole other issue. For those investors who are invested - in either direct or indirect ways - in the leverage loan markets or individual companies dependent on such loans, we advise caution. Sometimes the illusion created by fata morgana creates castles where none exist and that’s not a proper defense for anybody’s investments.

RSS Feed

RSS Feed