“I remember watching cartoons as a kid where each character had a super power. Some could fly, some could see through walls, some shot sticky crap to catch the bad guys. They all had something that innately made them better than both the bad guys and the good guys. When I’m looking at a potential investment, I want my managers to have capital allocation super powers. I want the Superman of return on capital”.

- Allard Ross

“It’s interesting. I’ve never found a single test that can help you find a manager that - over the long-term - has the uncanny ability to be an outstanding allocator of capital. Perhaps the one and only corelative factor I’ve ever seen (and I mean this quite seriously) is whether the individual does their shopping at discount or second-hand stores. That nearly always guarantees you’ve got someone at the helm that takes shareholder capital very, very seriously.”

- Pierre Pontet-Canet

There was a story about Bob Kierlin, the former CEO of Fastenal (FAST) who used to buy his suits not a mark-down suit store, but suits already used by the manager at the mark-down suit store. He said, “Luckily, we're the same size. I picked up six of those suits for 60 bucks each." Another time, Bob and current CEO Dan Florness had to get to Chicago for a meeting. Since the meeting wasn’t until the next day, they decided to scrap the one-hour flight and drive instead – saving the company 78% in costs and eating at A&W because they had the cheapest hamburger on the route. But it wasn’t just frugality that Kierlin built into corporate DNA. Fairness was another. When a recession hurt Fastenal growth in 2001, management were the first to cut their pay. Variable pay for management declined 30%. Bob’s salary was hit the hardest. His $121,000 salary was cut almost in half to $63,500. For other employees, variable pay increased 4%.

Cheap Management Generate High Returns

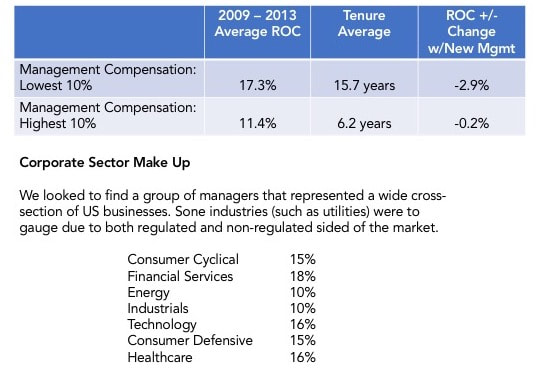

In 2014, Nintai Partners did an analysis comparing corporate return on capital of companies with management compensation in the highest decile versus companies with management compensation in the lowest decile. We were interested in seeing whether there was a correlation between how much management was compensated and their respective company’s return on capital. We chose 36 companies from the top decile of the S&P 500 and 49 companies from the top decile of the Russell 3000 and calculated return on capital for the years 2009 - 2013. We chose the same amount for the lowest decile. In addition, we wanted to see if individuals who are compensated either dramatically more or less had a different tenure within their respective companies. Last, we were interested to see what happened to the company’s ROC after that management team had left. (The pool of candidates was smaller here simply because not everyone has left yet).

It turns out there was a strong correlation. The numbers seen below show that management who are compensated the least have a dramatic - and positive - impact on ROC. I should note this applied in every industry sector listed (in the Corporate Sector Make Up). The lowest 10% in compensation achieved an average ROC from 2009 – 2013 of 17.3%. The highest 10% compensated managers achieved a ROC of only 11.4%. Additionally, the lowest paid managers stayed on in their CEO position nearly 10 years longer. As an investor, not only does your holding managed by the lowest compensated managers generate a higher ROC, but it achieves it for a longer period of time. Last, the departure of the lowest paid CEOs had a slight greater negative impact than the departure of the highest paid (this is to be expected since the gap was so large to begin with).

- Allard Ross

“It’s interesting. I’ve never found a single test that can help you find a manager that - over the long-term - has the uncanny ability to be an outstanding allocator of capital. Perhaps the one and only corelative factor I’ve ever seen (and I mean this quite seriously) is whether the individual does their shopping at discount or second-hand stores. That nearly always guarantees you’ve got someone at the helm that takes shareholder capital very, very seriously.”

- Pierre Pontet-Canet

There was a story about Bob Kierlin, the former CEO of Fastenal (FAST) who used to buy his suits not a mark-down suit store, but suits already used by the manager at the mark-down suit store. He said, “Luckily, we're the same size. I picked up six of those suits for 60 bucks each." Another time, Bob and current CEO Dan Florness had to get to Chicago for a meeting. Since the meeting wasn’t until the next day, they decided to scrap the one-hour flight and drive instead – saving the company 78% in costs and eating at A&W because they had the cheapest hamburger on the route. But it wasn’t just frugality that Kierlin built into corporate DNA. Fairness was another. When a recession hurt Fastenal growth in 2001, management were the first to cut their pay. Variable pay for management declined 30%. Bob’s salary was hit the hardest. His $121,000 salary was cut almost in half to $63,500. For other employees, variable pay increased 4%.

Cheap Management Generate High Returns

In 2014, Nintai Partners did an analysis comparing corporate return on capital of companies with management compensation in the highest decile versus companies with management compensation in the lowest decile. We were interested in seeing whether there was a correlation between how much management was compensated and their respective company’s return on capital. We chose 36 companies from the top decile of the S&P 500 and 49 companies from the top decile of the Russell 3000 and calculated return on capital for the years 2009 - 2013. We chose the same amount for the lowest decile. In addition, we wanted to see if individuals who are compensated either dramatically more or less had a different tenure within their respective companies. Last, we were interested to see what happened to the company’s ROC after that management team had left. (The pool of candidates was smaller here simply because not everyone has left yet).

It turns out there was a strong correlation. The numbers seen below show that management who are compensated the least have a dramatic - and positive - impact on ROC. I should note this applied in every industry sector listed (in the Corporate Sector Make Up). The lowest 10% in compensation achieved an average ROC from 2009 – 2013 of 17.3%. The highest 10% compensated managers achieved a ROC of only 11.4%. Additionally, the lowest paid managers stayed on in their CEO position nearly 10 years longer. As an investor, not only does your holding managed by the lowest compensated managers generate a higher ROC, but it achieves it for a longer period of time. Last, the departure of the lowest paid CEOs had a slight greater negative impact than the departure of the highest paid (this is to be expected since the gap was so large to begin with).

Why This Matters

Anecdotally, I’ve often heard that if someone manages your money like their own then you’ve found a good manager. It turns out the data show that managers who are frugally compensated have a tendency to generate much higher return on capital than those who are lavishly compensated. I believe Nintai’s research can teach investors several lessons.

Frugality is a Lifestyle

It turns out frugality runs through many managers’ personal and professional lives. Whether it be Bob Kierlin at Fastenal or Ken Iverson at Nucor (NUE), some individuals run a tight financial ship throughout their lives. This type of tight-fisted approach to spending can run through an entire business creating extraordinary internal returns (such as return on capital, return on equity, and return on assets) as well as investor returns.

Frugal Managers are Long-Lived Managers

During their research, Nintai Partners wasn’t able to measure the happiness or contentment of low-compensated versus high-compensated managers. But one thing was for certain - managers who faithfully showed up on the lowest compensated list year after year remained at their post far longer than those who were the highest compensated.

Frugal DNA Remains Within the Organization

While return on capital decreased slightly after the departure of a lowest compensated manager, generally the company continued to outperform companies with the highest compensated managers. This persisted over the next 5 - 10 years in nearly every case. The values of the cheap-skate CEO had a lasting effect.

Conclusions

Over my investing career, I’ve always looked for companies with high return on capital because I believe these are organizations with the best chance at becoming (or already being) compounding machines. Partnering with managers whose personal and professional characteristics help drive high return on capital and receive low compensation can increase your chances in investing in one of these compounding machines. For instance - from 1987 to the 2019 - the S&P 500 has grown 989% while Fastenal’s stock has grown 49,000%. As an investor, you can’t ask for more than that. If you were Bob Kierlin, you simply didn’t.

DISCLOSURE: I own Fastenal in several accounts I personally manage.

Anecdotally, I’ve often heard that if someone manages your money like their own then you’ve found a good manager. It turns out the data show that managers who are frugally compensated have a tendency to generate much higher return on capital than those who are lavishly compensated. I believe Nintai’s research can teach investors several lessons.

Frugality is a Lifestyle

It turns out frugality runs through many managers’ personal and professional lives. Whether it be Bob Kierlin at Fastenal or Ken Iverson at Nucor (NUE), some individuals run a tight financial ship throughout their lives. This type of tight-fisted approach to spending can run through an entire business creating extraordinary internal returns (such as return on capital, return on equity, and return on assets) as well as investor returns.

Frugal Managers are Long-Lived Managers

During their research, Nintai Partners wasn’t able to measure the happiness or contentment of low-compensated versus high-compensated managers. But one thing was for certain - managers who faithfully showed up on the lowest compensated list year after year remained at their post far longer than those who were the highest compensated.

Frugal DNA Remains Within the Organization

While return on capital decreased slightly after the departure of a lowest compensated manager, generally the company continued to outperform companies with the highest compensated managers. This persisted over the next 5 - 10 years in nearly every case. The values of the cheap-skate CEO had a lasting effect.

Conclusions

Over my investing career, I’ve always looked for companies with high return on capital because I believe these are organizations with the best chance at becoming (or already being) compounding machines. Partnering with managers whose personal and professional characteristics help drive high return on capital and receive low compensation can increase your chances in investing in one of these compounding machines. For instance - from 1987 to the 2019 - the S&P 500 has grown 989% while Fastenal’s stock has grown 49,000%. As an investor, you can’t ask for more than that. If you were Bob Kierlin, you simply didn’t.

DISCLOSURE: I own Fastenal in several accounts I personally manage.

RSS Feed

RSS Feed