“When the markets crash, how do you discern between a good stock and a bad stock? Is it total returns? Is it beta relative to the general markets? Or is it something quite different, quite deeper in nature? Is it about the company and not the stock?”

“We spend a lot of time looking for systemic risk; in truth, however, it tends to find us."

I think investors make a terrible mistake when they ask “what’s a great stock to own during a bear market?”. One thing you want to own during a bear market is a great company, not necessarily a great stock. In fact, it might be a great company AND a terrible stock. Great companies really show their star qualities when the capital markets crash. They have tendency to not need access to the capital markets, they continue to excel at superb allocation of capital skills, and they use the tough times to invest in future profitable growth (note I say profitable). They don’t build empires, they build better businesses with wider moats.

Over time I’ve come to realize that great companies might not prevent losses in time of capital market crashes, but they often prevent permanent loss of capital during those times. In these last weeks of 2018, investors have fervently looked for the best means at avoiding such grievous losses. Great companies have some common attributes that allow investors to avoid those catastrophic losses which cripple long-term returns. Several of these are an ability to access to capital markets, outstanding capital allocation (even in downturns), and using tough times to increase long-term profitability and growth.

Access to Capital Markets

There’s an old saying that says only borrow money when you don’t need it. A tremendous number of investors found out in 2007-2009 that some of their core holdings were wholly dependent upon short term paper to survive and to conduct daily operations. Think of Bear Stearns or Lehman Brothers. Companies that survive – and even thrive – in bear markets are those that borrow only when they don’t need it. A great example of this is the difference between Goldman Sachs (GS) and Berkshire Hathaway (BRK.A) in the 2007-2009 market crisis. Goldman was forced to go to Warren Buffett with hat in hand and proffer a truly outstanding convertible debt offer to Berkshire to show Wall Street it had the capability to conduct business in a system under such stress.

The Ability to Keep Up Outstanding Allocation of Capital

In 2011 my old firm Nintai Partners did a study on return on capital in the technology sector during the 2007-2009 market crash. During that time frame, the top 100 technology companies by market cap saw their return on capital drop by roughly 40-45% in that 48-month period. On average it took roughly 24-36 months to recover their previous (higher) returns on capital. These numbers reflect a substantial hit to the very business structure and strategy when the capital markets swooned. Businesses with deep competitive moats, robust and reactive corporate strategies, and outstanding management were able to ride out these difficult times with little or no impact to their return on capital.

Use Difficult Times to Build Long Term Profitability

Great companies have the sense to use down times in the economy and markets (which frequently go together) to make investments for sustainable – and profitable – growth in the future. Whether it is maintaining budget levels in research and development or completing bolt-on acquisitions at reasonable prices, great management teams find ways to use depressed market prices or economic slow downs to further build on to their competitive advantages and moat.

A Working Example

An example of a company that meets these criteria is a long term holding of mine (both in the Nintai Charitable Trust as well as individual client accounts) – Manhattan Associates (MANH). Manhattan Associates is a software solutions provider to manage supply chains, inventory, and omni-channel operations for retailers, wholesalers, and manufacturers. Its supply chain services provide tools to manage transportation costs. The omni-channel solutions provide a central platform to manage inventory availability across channels. The inventory solutions provide distributions the ability to forecast inventory demand and plan future investments. The software plays a vital role in inventory management, production scheduling, and enterprise resource planning.

MANH is the prototypical type of company that I’ve invested in all my career. Revenue has grown roughly 14% annually over the past 10 years. Free cash flow and earnings have grown 22% and 23% respectively over the same period. The company has no short or long-term debt. The company is a free cash flow giant converting roughly one-quarter of every dollar in revenue to free cash. All of these statistics help illustrate a story of an extremely profitable company that steadily uses bull and bear markets to solidify its competitive position, balance sheet strength, internal operations, and overall gross and net margins.

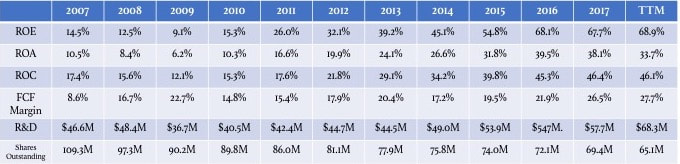

One example is Manhattan Associate’s outstanding share count. Going from 130.400,000 shares in 2003, the company has reduced these by over one-half with only 65,100,000 shares trading in late 2018. Another is Manhattan’s growth of 14.5% return on equity in 2007 to 68.9% in 2018. Even during the height of the Great Recession in 2008-2010, MANH generated free cash flow ratios of 16.7%, 22.7% and 14.8% respectively. During that same period, the company only slightly reduced their R&D budget spending $48.4M, $36.7M, and $40.5M respectively. Additional figures are seen below.

- Alex Beauharnais

“We spend a lot of time looking for systemic risk; in truth, however, it tends to find us."

- Meg McConnell

I think investors make a terrible mistake when they ask “what’s a great stock to own during a bear market?”. One thing you want to own during a bear market is a great company, not necessarily a great stock. In fact, it might be a great company AND a terrible stock. Great companies really show their star qualities when the capital markets crash. They have tendency to not need access to the capital markets, they continue to excel at superb allocation of capital skills, and they use the tough times to invest in future profitable growth (note I say profitable). They don’t build empires, they build better businesses with wider moats.

Over time I’ve come to realize that great companies might not prevent losses in time of capital market crashes, but they often prevent permanent loss of capital during those times. In these last weeks of 2018, investors have fervently looked for the best means at avoiding such grievous losses. Great companies have some common attributes that allow investors to avoid those catastrophic losses which cripple long-term returns. Several of these are an ability to access to capital markets, outstanding capital allocation (even in downturns), and using tough times to increase long-term profitability and growth.

Access to Capital Markets

There’s an old saying that says only borrow money when you don’t need it. A tremendous number of investors found out in 2007-2009 that some of their core holdings were wholly dependent upon short term paper to survive and to conduct daily operations. Think of Bear Stearns or Lehman Brothers. Companies that survive – and even thrive – in bear markets are those that borrow only when they don’t need it. A great example of this is the difference between Goldman Sachs (GS) and Berkshire Hathaway (BRK.A) in the 2007-2009 market crisis. Goldman was forced to go to Warren Buffett with hat in hand and proffer a truly outstanding convertible debt offer to Berkshire to show Wall Street it had the capability to conduct business in a system under such stress.

The Ability to Keep Up Outstanding Allocation of Capital

In 2011 my old firm Nintai Partners did a study on return on capital in the technology sector during the 2007-2009 market crash. During that time frame, the top 100 technology companies by market cap saw their return on capital drop by roughly 40-45% in that 48-month period. On average it took roughly 24-36 months to recover their previous (higher) returns on capital. These numbers reflect a substantial hit to the very business structure and strategy when the capital markets swooned. Businesses with deep competitive moats, robust and reactive corporate strategies, and outstanding management were able to ride out these difficult times with little or no impact to their return on capital.

Use Difficult Times to Build Long Term Profitability

Great companies have the sense to use down times in the economy and markets (which frequently go together) to make investments for sustainable – and profitable – growth in the future. Whether it is maintaining budget levels in research and development or completing bolt-on acquisitions at reasonable prices, great management teams find ways to use depressed market prices or economic slow downs to further build on to their competitive advantages and moat.

A Working Example

An example of a company that meets these criteria is a long term holding of mine (both in the Nintai Charitable Trust as well as individual client accounts) – Manhattan Associates (MANH). Manhattan Associates is a software solutions provider to manage supply chains, inventory, and omni-channel operations for retailers, wholesalers, and manufacturers. Its supply chain services provide tools to manage transportation costs. The omni-channel solutions provide a central platform to manage inventory availability across channels. The inventory solutions provide distributions the ability to forecast inventory demand and plan future investments. The software plays a vital role in inventory management, production scheduling, and enterprise resource planning.

MANH is the prototypical type of company that I’ve invested in all my career. Revenue has grown roughly 14% annually over the past 10 years. Free cash flow and earnings have grown 22% and 23% respectively over the same period. The company has no short or long-term debt. The company is a free cash flow giant converting roughly one-quarter of every dollar in revenue to free cash. All of these statistics help illustrate a story of an extremely profitable company that steadily uses bull and bear markets to solidify its competitive position, balance sheet strength, internal operations, and overall gross and net margins.

One example is Manhattan Associate’s outstanding share count. Going from 130.400,000 shares in 2003, the company has reduced these by over one-half with only 65,100,000 shares trading in late 2018. Another is Manhattan’s growth of 14.5% return on equity in 2007 to 68.9% in 2018. Even during the height of the Great Recession in 2008-2010, MANH generated free cash flow ratios of 16.7%, 22.7% and 14.8% respectively. During that same period, the company only slightly reduced their R&D budget spending $48.4M, $36.7M, and $40.5M respectively. Additional figures are seen below.

Have all these attributes saved the company from poor returns over the last year? Absolutely not. Through December 24 2018, the stock’s year-to-date return has been down -17%. Its 5-year cumulative return through 2018 has been only 32%. Owning a company such as Manhattan Associates doesn’t guarantee you great returns over the short or medium term. But I would argue the characteristics of the company – from management’s capital allocation skills to its balance sheet strength – provide an opportunity to reduce your chances at permanent capital impairment during a bear market.

Conclusions

I have written over the years that the outperformance of my Nintai Partners and Dorfman Value Investment (neither of which I personally manage any more) portfolios has been about losing less in bear markets rather than making more in bull markets. This recent bear market reinforces my thesis with my individual managed portfolios at Nintai Investments LLC losing roughly -4.5% YTD versus the S&P 500’s -12.8% through December 24 2018. As Beauharnais said, purchasing great companies (along with not overpaying or holding cash) can make all the difference in a bear market. The companies in my portfolios – like Manhattan Associates - make downside protection a priority. By seeking out such companies yourself, you might not just ride out a bear market with better results but also sleep better at night.

Conclusions

I have written over the years that the outperformance of my Nintai Partners and Dorfman Value Investment (neither of which I personally manage any more) portfolios has been about losing less in bear markets rather than making more in bull markets. This recent bear market reinforces my thesis with my individual managed portfolios at Nintai Investments LLC losing roughly -4.5% YTD versus the S&P 500’s -12.8% through December 24 2018. As Beauharnais said, purchasing great companies (along with not overpaying or holding cash) can make all the difference in a bear market. The companies in my portfolios – like Manhattan Associates - make downside protection a priority. By seeking out such companies yourself, you might not just ride out a bear market with better results but also sleep better at night.

RSS Feed

RSS Feed